On Melbourne Cup Day, 2024 the RBA announced that interest rates would remain on hold, leaving the cash rate at 4.35%. Accompanied with this announcement was some explanation of why the rates did not change and that changes are unlikely in the short term.

The RBA explained that part of the decline in inflation was a result of temporary government strategies such as providing relief to high electricity costs, thus keeping inflation down. But when these strategies were lifted, inflation was likely to rise and be above the target rate of 2.5%-3%. The target rate is not expected to reach 2.5% until late 2026.

As I was driving this morning, a radio commentator gave a very simple example of what forces are at play when it comes to changes in the cash rate. If you take the building industry, the number of applications for new buildings is decreasing as the economy slows. However, those builders who have work find that the cost of supplies is rising due to a shortage of product and a shortage of labour. These two elements are increasing the cost of building while the demand for housing is decreasing.

Experts would agree that most predictions do not eventuate. If the experts can’t get it right, what chance does the consumer have.

Most people will not have experienced the high home loan costs of over 15% that occurred in the late 1980s. In 1990, the home loan rate peaked at 17.5%. While increases to this level are unlikely, some of the current borrowers would be financially stressed if interest costs were to rise by 2%. This graph displays the Standard Variable Home Loan Rates since the Year 2000.

A 2% increase could mean some borrows on variable interest rates could be looking of rates at about 10%. How would your personal budget handle such an event?

An often-quoted phrase is:

Hope for the best, but prepare for the worst

Financial Mappers

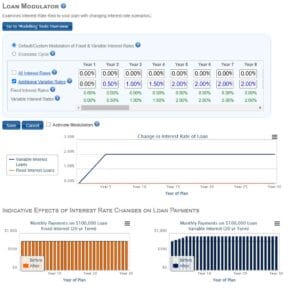

Financial Mappers can help you prepare for the worst by using its extensive list of modelling tools. In the example below, Variable Interest Rates rise by 0.5% each year for 4 years. The dark blue columns show the increase in Monthly Payments on a $100,000 loan.

Review your Living Expenses Budget to work out what are your Optional Expenses and see what costs you can go without. It may be your extra take-away or movie night that must go. Alternatively, you may have to do some more overtime, take a second part-time job. Financial Mappers will even create a report showing your cash flows without and without Optional Expenses.

You may also need to calculate at what interest rate, you can no longer afford to make your home loan payments. This may be the time when you must consider selling. If that is the case, you are unlikely to be alone, meaning there are more sellers than buyers. In that situation, house prices may fall.

There are ways you can cushion yourself against these unexpected interest rate rises without having to fix the interest rate. Fixed Interest Rates are usually higher than variable ones.

Consider the following:

- Create an Emergency Cash Account, where the balance is sufficient to cover increased loan payments for a year or two.

- If your lender will allows, increase your loan payments so that your balance is always in advance. Check that your lender will allow you to use these additional payments to offset loan costs.

- When you take out a loan, work out what the loan payments would be if you wanted to repay it in 5 years less than the loan time. Increase your loan payments to that amount. Again check with the lender to ensure they will allow the advanced payments to cover any increase in interest rates.

Financial Mappers is designed to allow everyone to create a financial plan and then consider what if scenarios should the economy take a turn for the worst.

Glenis Phillips SF Fin – Designer of Financial Mappers

Disclaimer: Financial Mappers does not have an Australian Services License, does not offer financial planning advice, and does not recommend financial products.